5th Floor, West Tower, World Financial Centre

1 Dong San Huan Middle Road

Chaoyang District, Beijing 100020, China

Tel: +86 10 5081 5880

April 23, 2020

The Research Paper "Responding to Unexpected Global Disaster: Analysis on E ...

The COVID-19 pandemic has imposed an enormous and intensifying impact on the global society and economy. Major economies have been responding to the worldwide outbreak with extraordinary economic policies. In this regard, the team of China Academy of Financial Research (CAFR) at Shanghai Jiao Tong University (SJTU) recently released a report to systematically review and analyze the characteristics and development of the pandemic, its mechanism, transmission and actual impact on the global economy, as well as the policy responses, objectives and measures of major economies. It also provides a preliminary assessment and discussion of the effects and results of such policies. The report indicates the following findings: 1. COVID-19 is a unexpected global disaster. Unlike the endogenous economic recessions such as the Great Depression in 1929 and the global financial crisis in 2008, the pandemic is exogenous, while its development depends on global prevention and control, which reflects the transformation from an exogenous event to an endogenous one as well as the interaction between exogenous and endogenous elements. 2. The impact of COVID-19 on the society and its normal operation has caused the real economy to halt and has led to direct, comprehensive and enormous effects: (1) The demand has dropped significantly; (2) The supply has been greatly affected; (3) The financial market is in extensive tension and turbulence; and (4) All macroeconomic indicators have deteriorated, with increasing uncertainties. 3. During the evolution from a local outbreak to a pandemic, the responses of major economies have rapidly changed from "normal management" focusing on financial and economic stabilization, to "unusual responses" with the priority of COVID-19 prevention and control, while maintaining financial and economic stability. 4. The monetary, financial and fiscal policies of major economies concentrate on the goals of "1+5", that is: (1) to fight against COVID-19; (2) to protect people's livelihood; (3) to bail out businesses; (4) to stabilize the finance market; (5) to minimize the risk of an economic crisis; and (6) to guide the market to anticipate and prepare for economic recovery. These policies show the characteristics of "global emergency management", featuring continuous introduction, clear objectives, unprecedented intensity, abundant instruments (both conventional and unconventional), comprehensive coverage and national policy linkage. 5. Initial effects of the policies: (1) Direct financial supports for medical and healthcare resources, local finance, citizen assistance and corporate bailouts will extend 2-3 months, or even longer if necessary; (2) Financial markets are gradually stabilizing; (3) The effects of stabilizing the real economy and preventing economic crises will depend on the effectiveness of COVID-19 prevention and control efforts; and (4) The economic and financial policies of the governments have now played the expected role in stabilization to an extent. It is widely recognized that economic stability and recovery can only be possible after COVID-19 is completely under control, which will become the priority goal afterwards. 6. Specific and unusual responses call for direct intervention of the policies in the market, but in the long run, these interventions, including how they “exit”, will affect financial stability, macro leverage, fiscal policies, economic restructuring and to a deeper extent, conflicts in social structure, global spillover, macroeconomic policies and the relationship between the government and the market in many ways.

April 01, 2020

SAIF Held the Faculty and Staff Meeting of 2020 Spring Semester

On March 30th, Shanghai Advanced Institute of Finance (SAIF), Shanghai Jiao Tong University (SJTU) held the Faculty and Staff Meeting of 2020 Spring Semester. Prof. Guangshao Tu, Adjunct Professor of SJTU and Executive Director of SAIF, and Prof. Jiang Wang, Executive Director of SAIF and Chairman of SAIF Faculty Council, delivered speeches respectively. Prof. Chun Chang, Executive Dean of SAIF, and Prof. Qigui Zhu, Secretary of the CPC SAIF Committee, served as keynote speakers. Nearly 200 SAIF professors and staff attended the event on site or remotely.

March 18, 2020

SAIF Alumni Support the Fight Against COVID-19

After the outbreak of COVID-19, SAIF Alumni Association published a "Support Initiative" on January 27th, calling on all alumni to act immediately and do their best to make contributions to the people in Hubei and Wuhan, support the tough battle against the epidemic and overcome difficulties together with love and practice. The Initiative received a warm response from all SAIF alumni. Alumni clubs, classes and enterprises have been positively involved in the move. Statistics shows that as of now, 138 alumni or their companies and 9 classes have donated a total of RMB681 million in cash and materials worth hundreds of millions of RMB, including nearly 340,000 protective suits, 2.97 million masks, 1.36 million pairs of gloves, 1,500 pairs of goggles, 110 tons of medical alcohol, 3,350 tons of sodium hypochlorite disinfectant, 10,000 boxes of testing reagents, 2 anti-epidemic special sanitation vehicles, 1 high-temperature disinfection and anti-epidemic vehicle, 40 heat guns, 338 air purifiers , 30 medical ventilators, 200 negative pressure suction devices, 200 monitors and other daily supplies worth approximately RMB356 million.

March 02, 2020

SAIF Rings Its Class Bells on the “Cloud”!

On March 1st 2020, SAIF launched a number of cloud-based online courses. The first "Curriculum in March" covered 32 courses, of which 14 courses went alive for MBA and MF students in the first week, involving 17 classes and around 850 students. In addition to the new hardware system, the changes in the form of teaching also posed challenges to the faculty. In this regard, Prof. Hong Yan, Deputy Dean of SAIF, explained, "Before the start of the curriculum, we have conducted several rounds of communication with all the involved professors, who have adjusted the forms of teaching and added the parts of online interaction and Q&As. The trial lectures were also executed in advance. The only purpose is to prevent the potential deterioration of teaching quality due to changes in the teaching forms." More than 70% of the 32 courses launched in March used live streaming technology. The faculty also provided online tutoring to students through after-class interactive communication and Q&A. Though the COVID-19 temporarily prevents SAIF students from returning to campus, it couldn’t stop their dedication to study, not to mention the commitment and efforts made by SAIF faculty and staff. With the joint efforts, the class bells rang in the cloud will surely be the most beautiful sound in this special spring.

January 30, 2020

SAIF Honored as "Top 100 Think Tanks to Watch" and "Top 100 Best ...

The Think Tanks and Civil Societies Program (TTCSP) of the Lauder Institute at the University of Pennsylvania released the "Global Go To Think Tank Index Report 2019 " on January 30th, 2020 (hereinafter referred to as the "Report"). The ranking of "Top 100 Think Tanks to Watch" lists four Chinese think tanks, including Shanghai Institute of Advanced Finance (SAIF), which also enters the list of "Top 100 Best Managed Think Tanks in 2019". It marks the 14th edition of the Report, which is one of the most authoritative reports of think tank research and development in the world. Through an objective and fair research system, it aims to engage in ongoing research and comprehensive ranking of global think tanks and review their roles in governments and society around the world, so as to strengthen the capacity building and improve the performance of worldwide think tanks. In 2019, of all the 8,248 think tanks catalogued in the TTCSP’s Global Think Tank Database, Europe features the most think tanks, with a total of 2,219 (26.9%). The number of Asian think tanks is the same as last year. China ranks as the third largest country in the world in terms of the quantity of think tanks (507). SAIF ranks No. 2 in China and No. 38 in the world in "Top 100 Think Tanks to Watch in 2019". In the list of " Top 100 Best Managed Think Tanks in 2019", SAIF ranks 40th in the world, only after the Development Research Center of the State Council (DRC) (31st in the world) among all Chinese peers. These highlights further prove that SAIF's research strength and role of a think tank have attracted worldwide attention.

January 23, 2020

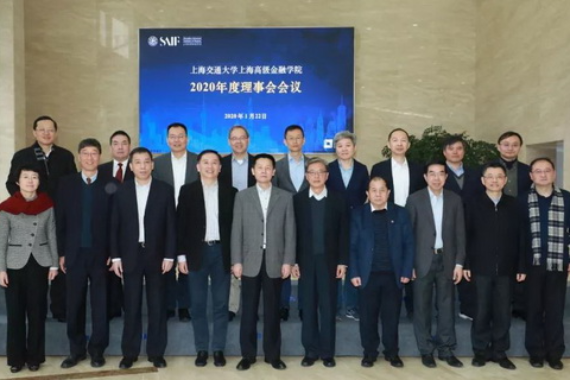

SAIF Held 2020 Annual Board Meeting

On January 22nd, 2020, Shanghai Advanced Institute of Finance (SAIF) held 2020 Annual Board Meeting at SAIF Xuhui Campus of Shanghai Jiao Tong University (SJTU). Qing Wu, Member of the Standing Committee of CPC Shanghai Municipal Committee, Vice Mayor of Shanghai and Chairman of SAIF, presided over the meeting and delivered a speech. Mingbo Chen, Deputy Secretary General of Shanghai Municipal Government and Deputy Chairman of SAIF; Jing Lu, Director of Shanghai Education Commission and Director of SAIF; Dong Xie, Director of Shanghai Financial Affairs Bureau and Director of SAIF; Sixian Jiang, Secretary of CPC Committee at SJTU and Deputy Chairman of SAIF; Zhongqin Lin, President of SJTU and Director of SAIF; Guangshao Tu, Adjunct Professor of SJTU and Executive Director of SAIF; Zhen Huang, Vice President of SJTU and Director of SAIF; and Jiang Wang, Chairman of SAIF Faculty Council and Executive Director of SAIF, attended the meeting. Qi Liang, Director of Human Resources Department of SJTU, Yaguang Wang, Dean of the Graduate School, Chun Chang, Executive Dean of SAIF, Qigui Zhu, Secretary of CPC SAIF Committee, and other SJTU department heads and senior professors were also present. At the meeting, Prof. Jiang Wang presented “2019 Annual Work Report” on behalf of SAIF Board. Chairman Qing Wu and other directors highly affirmed the progress and achievements made by SAIF over the past decade, in particular in 2019, and brainstormed ideas and suggestions for SAIF’s future development. They hoped that SAIF will review the feedback of recent international assessment, continue to adhere to the track of internationalization, specialization and market orientation, and build up a world-class financial school, in order to serve as an important academic support, talent highland and brand of Shanghai as an international financial hub, and make its contributions to the upgrading of Shanghai's urban energy level and core competency.

January 13, 2020

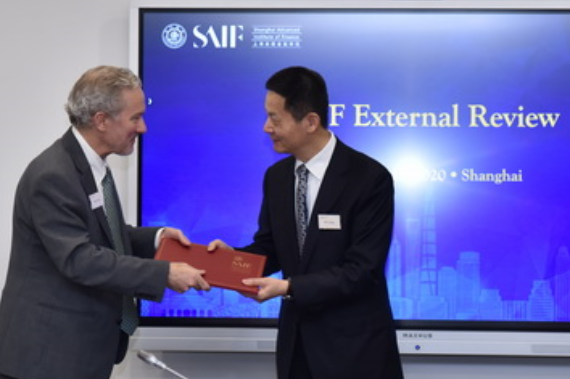

SAIF Completed Its Second International Evaluation

From January 10th to 11th, 2020, an International Evaluation Committee composed of six world-class experts and scholars from top-notch business schools visited Shanghai Advanced Institute of Finance (SAIF), Shanghai Jiao Tong University (SJTU) and conducted the second comprehensive evaluation on the development of SAIF over the past decade in terms of faculty development, talent training, research platform, school management, alumni relations and other dimensions. The International Evaluation Committee was chaired by Franklin Allen, Professor of Finance and Economics at the Imperial College London, former Deputy Dean of the Wharton School of the University of Pennsylvania and former Chairman of the American Finance Association. The other five experts included Kathleen Hagerty, Associate Provost at Northwestern University; Rich Lyons, former Dean and Professor of Finance of the Haas School of Business at the University of California, Berkeley; Maureen O'Hara, Robert W. Purcell Chair Professor of Finance at Johnson School of Management of Cornell University and former Chairman of the American Finance Association; Stephen Schaefer; Professor of Finance and former Associate Dean of London Business School and former Academic Director of AQR Institute of Asset Management; and Ernst-Ludwig von Thadden, former President and Professor of Microeconomics and Finance of the University of Mannheim. Qing Wu, member of the Standing Committee of CPC Shanghai Municipal Committee, Vice Mayor of Shanghai and Chairman of the SAIF Board, welcomed the International Evaluation Committee on behalf of SAIF Board and thanked the experts for their efforts and contributions on the two-day review. After carefully listening to the feedback from the committee, Qing Wu stated that the experts carried out “diagnostics" for SAIF’s development and the valuable suggestions put forward are very inspiring and helpful for SAIF to move forward. In the future, these useful opinions will be integrated into SAIF’s practice and drive SAIF’s advancement. He believed that with the ongoing attention and support of the experts, SAIF will better serve its mission, cultivate more outstanding financial professionals and contribute to the construction of Shanghai into an international financial hub as well as China's financial sector.

January 06, 2020

SAIF Attended ASSA for Young Faculty Recruitment

From January 2nd to 5th, 2020, the young faculty recruiting team of Shanghai Advanced Institute of Finance (SAIF), Shanghai Jiao Tong University (SJTU) attended the Allied Social Science Association Annual Meeting (ASSA) 2020 in San Diego to headhunt young international faculty via the American Finance Association (AFA). Global recruitment of world-class faculty has always been the focus of SAIF’s construction of an international faculty team. In order to benchmark top-notch business schools in North America, SAIF is the first to introduce the world's leading faculty recruitment system of Interfolio Faculty Search among business schools in China, to screen resumes more precisely and select outstanding talents more efficiently. During ASSA, the recruiting team composed of Prof. Jiang Wang, Chairman of SAIF Faculty Council, Prof. Chun Chang, Executive Dean of SAIF, Prof. Hong Yan, Deputy Dean of SAIF, Prof. Jun Pan, Chairman of the Recruiting Committee, and a few young professors conducted in-depth communication and conversation with dozens of candidates, and finalized the shortlist for the second round of interviews and campus visits.

December 10, 2019

IMF Released the World Economic Outlook and The Future of China's Bond Market at ...

The World Economic Outlook and The Future of China's Bond Market jointly sponsored by the International Monetary Fund (IMF) China Office, Shanghai Advanced Institute of Finance (SAIF), Shanghai Jiao Tong University and CBN Research Institute were released at SAIF recently. Mr. Alfred Schipke, Chief Representative of IMF in China, Ms. Longmei Zhang, Deputy Representative of IMF in China, Prof. Chun Chang, Professor of Finance and Executive Dean at SAIF, Prof. Min Zhu, Dean of the National Institute of Finance of Tsinghua University, Prof. Hong Yan, Professor of Finance and Deputy Dean for Faculty and Research at SAIF, and Mr. Changchun Hua, Chief Economist of Guotai Junan Securities attended the event. The release is a showcase of cutting-edge findings in economic research and an exchange of views jointly created by SAIF, IMF and CBN Research Institute. In the future, SAIF will always be committed to the cultivation of high-end financial talents and high-level research in financial disciplines, further enhance the breadth and depth of exchanges and cooperation with top research institutions at home and abroad, grasp the pulse of the world economy, and serve China's economic development.

November 27, 2019

SAIF and CCB Fund Signed Comprehensive Strategic Cooperation Agreement

On November 20th, 2019, Shanghai Advanced Institute of Finance (SAIF), Shanghai Jiao Tong University and CCB Fund signed a strategic cooperation agreement at SAIF Xuhui Campus. Sun Zhichen, Chairman of CCB Fund, attended the ceremony, along with Prof. Chun Chang, Executive Dean at SAIF, Prof. Feng Li, Associate Director of China Academy of Financial Research (CAFR) and Co-Director of Shanghai Advanced Institute for Financial Research (SAIFR), Prof. Xiaokang Yang, Executive Vice President of the Artificial Intelligence Institute at Shanghai Jiao Tong University, Prof. Hong Yan, Deputy Dean for Faculty and Research at SAIF, Prof. Jie Pan, Associate Dean at SAIF, and Prof. Xianglin Li, Associate Director of CAFR and Director of FinTech Research Center. According to the agreement, the two parties aim to strengthen the FinTech capabilities of CCB Fund to the greatest extent and use FinTech as its core driving force to continuously improve its capabilities of investment, customer services, product innovation, risk management and value creation. They will also create an innovation research base and closely integrate cutting-edge technologies with industry trends and practice. The two parties will create an open academic research platform to explore research cooperation on application-oriented topics, cultivate talents that meet the needs of the industry, solve practical problems, serve the structural transformation and drive the prosperity of the industry. This strategic cooperation is regarded as a valuable practice of "joint innovation" in academia and investment.

211 West Huaihai Road

Shanghai 200030, China

Tel: +86 21 6293 3500

9th Floor, Building T6, Hongqiao Hui

990 Shenchang Road

Shanghai 201106, China

5th Floor, West Tower, World Financial Centre

1 Dong San Huan Middle Road

Chaoyang District, Beijing 100020, China

Tel: +86 10 5081 5880

1203 Tower 7, One Shenzhen Bay

Nanshan District, Shenzhen 518000, China

Tel: +86 755 8663 8815

© Shanghai Advanced Institute of Finance All Rights Reserved.

Top