In line with China's commitment to the global community to combat climate change, the Central Committee of the Communist Party of China and the State Council issued "Guidelines for Full and Faithful Implementation of the New Development Philosophy and the Planning of Carbon Peaking and Carbon Neutrality" on October 24, 2021. This plan outlines China's systematic approach to achieving carbon peaking and carbon neutrality.

The Shanghai Advanced Institute of Finance (SAIF) is committed to contributing to China's national development and the global community's sustainable development. SAIF has set a long-term goal to become a world-class institution of research and advanced learning in finance and management, with a focus on Chinese markets and their global connections. SAIF recognizes that sustainability is at the core of China's new development philosophy and that carbon peaking and carbon neutrality are critical to solving environmental problems and promoting sustainable development.

As an educational institute, SAIF recognizes its critical role in providing intellectual leadership in decarbonization and sustainable development. SAIF scholars have actively engaged in research and policy advice related to carbon emission reduction and broader issues related to the link between environmental change, social responsibility, corporate governance, financial behavior, and financial markets. Their research outcomes have been published in international journals. SAIF has also established the Center for Sustainable Investment to collaborate extensively with the financial industry and governments at all levels. As policy advice, SAIF has actively participated in the formulation of a number of green finance laws and regulations. It has helped develop important products such as the Shanghai Green Finance Index. Additionally, SAIF offers ESG-related courses, which have contributed to educating finance professionals in low carbon and sustainability.

SAIF has explored its own path for green development and taken the construction of a low-carbon campus as a key long-term goal. SAIF has formulated detailed carbon reduction goals and action plans and aims to achieve carbon peaking by 2030 and carbon neutrality by 2045. Carbon footprint accounting, as an indicator used to evaluate an organization's impact on climate change, helps SAIF understand its current carbon and sustainability status, identify areas for improvement and innovation, and establish carbon reduction targets and a low-carbon roadmap.

Carbon Reduction Target and Roadmap Planning

Consistent with the overall strategic goal of China’s national sustainable development, we regard serving the national and global goal of mitigating climate change as one of our long-term strategic goals. The current carbon reduction target and roadmap planning marks an essential step taken by SAIF in the direction of green economy and low carbon emissions. With our commitment to ameliorate our planet’s environmental strains through practical action, SAIF will find scientific, robust and rational methods to achieve low carbon emissions and sustainability. Using this knowledge, we will then create an action plan for carbon reduction to facilitate the construction of a low-carbon business school.

Based on our carbon emissions from 2019 to 2022, along with further feasibility analysis, Shanghai Advanced Institute of Finance at Shanghai Jiao Tong University aims to achieve carbon peaking by 2030 and carbon neutrality by 2045.

To achieve these goals, SAIF will continue to implement carbon reduction roadmap planning through "low-carbon soft environment construction" and "low-carbon hard environment construction." As to the former, SAIF will continue to improve its carbon emission management system, its low-carbon and sustainable development work plan, and its archives for low-carbon campus creation. We will incorporate carbon emission budgeting and accounting into our overall financial system, train low-carbon volunteers, and strengthen the initiative for low-carbon energy conservation.

As to the latter, SAIF will optimize carbon emission management for campus buildings and centers, increase energy savings and emissions reduction through the renovation of facilities, and explore low-carbon operations teaching. SAIF will provide more intellectual support for exploring the strategies of carbon peaking and carbon neutrality in theoretical research, empirical analysis, and practical tests.

2022 Carbon Footprint Accounting

As an indicator in assessing an organization's response to climate change, the carbon footprint accounting enables a clear understanding of the current state of the organization's low-carbon and sustainable development, and identifies areas for improvement and innovation. By leveraging rational and scientific planning, organizations can set emission reduction targets as well as a low-carbon roadmap.

As an initial step in devising a carbon reduction roadmap and formulating a carbon reduction action plan, SAIF is adopting a scientific carbon emissions model to calculate its carbon footprint for its Shanghai campus, Beijing Center, and Shenzhen Center. This analysis will serve as a foundation for establishing SAIF's carbon reduction goals and constructing a low-carbon institute.

SAIF’s carbon footprint accounting goals and technical approach are outlined, as follows.

Carbon Footprint Accounting Goals

• Calculate the carbon footprint of the main emission sources within the boundaries of SAIF's Shanghai campus, Beijing Center, and Shenzhen Center.

• Use the establishment of a low-carbon institute as the starting point to further enhance efforts toward achieving a "Dual Carbon" goal.

Carbon Footprint Accounting Technical Approach and Results

I. Reference

The carbon accounting method adopted in this report is calculated in accordance with "A Corporate Accounting and Reporting Standard" (The Greenhouse Gas Protocol) and refers to the "Specification with Guidance at the Organization Level for Quantification and Reporting of Greenhouse Gas Emissions and Removals” (ISO 14064-1:2018) guidelines, described, as follows.

1) The Greenhouse Gas Protocol. Established jointly by the World Resources Institute (WRI) and the World Business Council for Sustainable Development (WBCSD), it develops internationally recognized greenhouse gas accounting, reporting methods, and standards. The revised version, which was published in 2009, has been widely recognized internationally.

2) ISO 14064-1:2018. ISO 14064 was published by the International Organization for Standardization (ISO) in 2006, consisting of three parts: enterprise-level carbon accounting (ISO 14064-1), project-level carbon accounting (ISO 14064-2), and greenhouse gas verification (ISO 14064-3). ISO 14064-1 is the internationally recognized standard for organization-level carbon accounting, and our report refers to its latest edited 2018 version.

II. Establish the Organizational Boundary

To set SAIF’s carbon footprint accounting boundary, an accounting method is chosen in accordance with international standards, and the selected method is then used to define the emission activities of the institution. As the subject of the carbon footprint accounting is the Shanghai Advanced Institute of Finance, a public institution, the Control Approach is used to set the organizational boundary and consolidate the carbon footprint accounting results.

III. Establish Operational Boundaries

According to "A Corporate Accounting and Reporting Standard" (The Greenhouse Gas Protocol) and reference to the "Specification with Guidance at the Organization Level for Quantification and Reporting of Greenhouse Gas Emissions and Removals” (ISO 14064-1:2018) guidelines, three “scopes” (scope 1, scope 2, and scope 3) are defined for carbon accounting and reporting purposes, as follows.

• Scope 1: Direct GHG emissions occur from sources that are owned or controlled by the organization, such as carbon emissions generated by boilers, vehicles, and refrigerant leaks from air conditioners that SAIF owns or controls.

• Scope 2: Indirect GHG emissions generated by purchased electricity and heat consumed by the organization.

• Scope 3: Other Indirect GHG emissions which are a consequence of the activities of the organization but occur from sources not owned or controlled by the organization. Scope 3 emissions are divided into 15 categories.

Taking into account the conditions of SAIF’s daily operation, we have defined the operational boundaries for SAIF’s carbon accounting. Specifically, scope 1 emissions include fuel consumption by vehicles owned by the institute, as well as emissions caused by refrigerant leaks in air conditioning. Scope 2 emissions include the electricity used by the institute. After analyzing the representative categories within Scope 3, we selected Category 1 (Purchased Goods and Services), Category 6 (Business Travel), and Category 7 (Employee Commuting) for disclosure in this report.

IV. Determination of Greenhouse Gas Reporting Categories

Seven greenhouse gases are annotated by ISO 14064-1: 2018. These include: CO2, CH4, N2O, HFCs, PFCs, SF6, and NF3. SAIF's carbon footprint accounting will include these seven greenhouse gases and will ultimately be calculated, and reported, in units of carbon dioxide equivalent.

V. Emission Factors

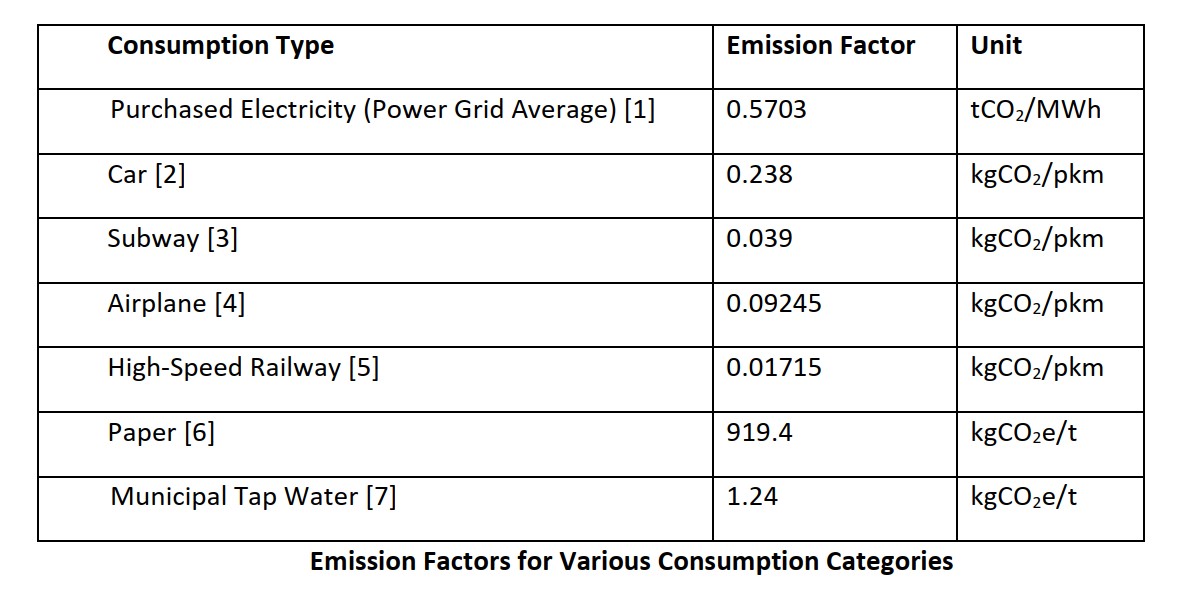

Carbon emissions incurred by a specific emission source, such as purchased electricity and thermal, are usually calculated based upon published emission factors. The sources of emission factor data are arranged in order of authoritativeness: emission factors officially published by the government, factors disclosed by industry experts, professional organizations, and research reports. To ensure the authoritativeness of the carbon footprint accounting, the following emission factors were selected.

[1] Source: Ministry of Ecology and Environment of the People’s Republic of China

[2] Source: Carbon Accounting Methodology for Carbon Reduction Trips, Beijing

[3] Source: Beijing Low-Carbon Travel Methodology

[4] Source: Large-Scale Conferences and Exhibitions Low-Carbon Assessment Guidelines

[5] Source: Large-Scale Conferences and Exhibitions Low-Carbon Assessment Guidelines

[6] Source: CPCD

[7] Source: Ecoinvent

VI. Quantify Carbon Emissions

After defining the scope of analysis for SAIF's carbon footprint in 2022, identifying all major sources of greenhouse gas (GHG) emissions, and collecting activity data, the physical emissions of various sources were converted into "carbon dioxide equivalent".

Carbon dioxide is the primary gas produced by human activities that contributes to the greenhouse effect. Other greenhouse gases have varying contributions to the Earth's greenhouse effect. To measure overall impacts uniformly, carbon dioxide equivalent is generally used as the basic unit for measuring the greenhouse effect. The carbon dioxide equivalent of a greenhouse gas is obtained by multiplying its global warming potential (GWP) by its emission volume. This approach standardizes the effect of different greenhouse gases. The global warming potential is typically calculated based on 100 years and is represented as GWP100. For example, methane's GWP100 value is 27.9, indicating that the amount of heat captured by one metric ton of methane emitted over 100 years is 27.9 times that of one metric ton of carbon dioxide.

In practice, the activity data related to carbon emissions can be obtained directly, and the more direct calculation method involves converting the activity's carbon emissions into carbon dioxide equivalents using the emission factor. The emission factor refers to the average carbon dioxide emission per unit activity. The institute's carbon footprint is equal to the sum of the carbon dioxide equivalents generated by all activities or consumption related to carbon emissions.

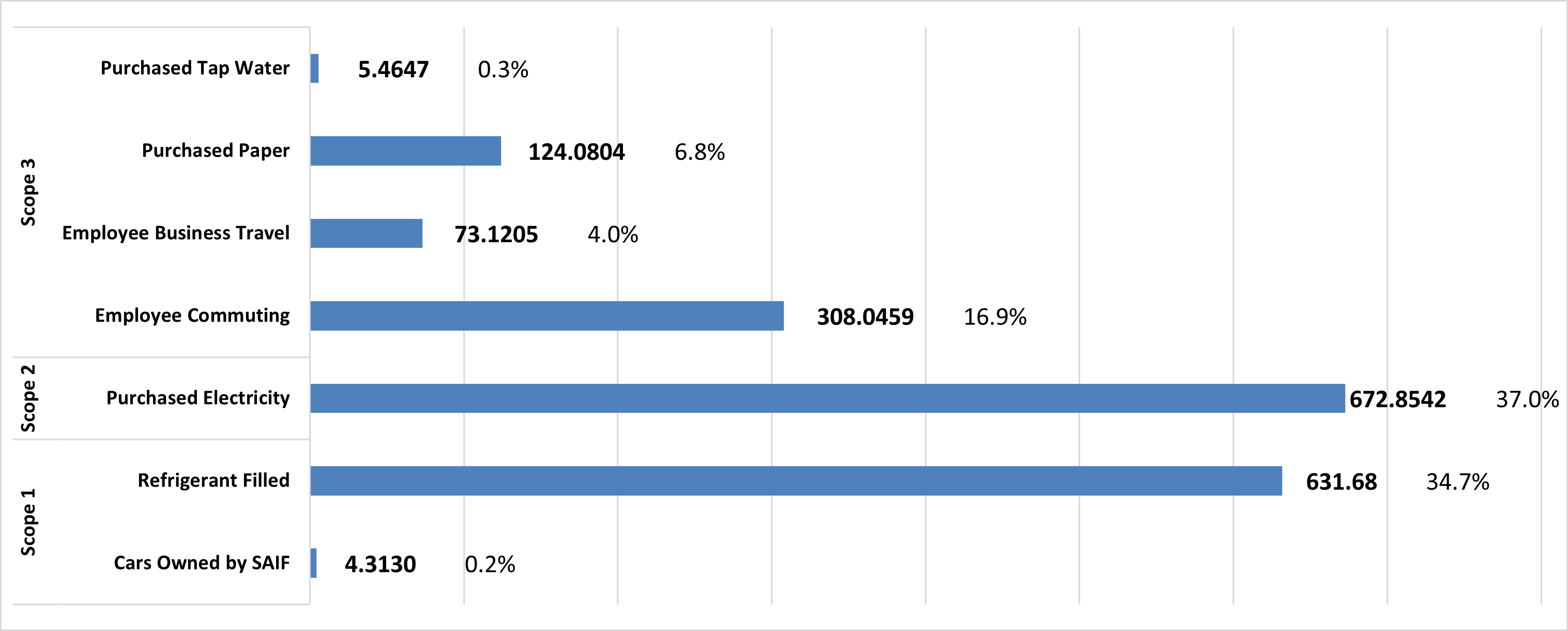

Based on the activity statistics and the above emission factors, we now have the following annual carbon emissions of SAIF during 2022.

Based on the results of carbon footprint accounting, SAIF's total carbon emissions in 2022 decreased by 263.461 tons of carbon dioxide equivalent compared to 2019. As the school anticipates an increase in teaching and faculty exchange activities as we emerge from the COVID-19 pandemic, SAIF will intensify its efforts to control various carbon emission factors, limit the total growth of carbon emissions, and achieve its carbon neutrality development goal.

(This summary is based on a third-party accounting report. If you require access to the full report, please contact the SAIF Dean’s Office.)